In recent years, investment funds have become an increasingly important component of Iran’s financial system, offering structured mechanisms for channeling capital toward productive sectors of the economy. These funds serve as intermediaries between investors and financial markets, enabling portfolio diversification, professional asset management and enhanced market efficiency. Despite being a relatively young segment compared to global counterparts, Iran’s investment fund industry has demonstrated substantial growth in both scale and sophistication. HOSSEIN JALILINIA examines the development and structure of investment funds in Iran.

By contextualizing Iran’s investment funds within both domestic financial reforms and global investment trends, this study seeks to contribute to a deeper understanding of how collective investment vehicles function as instruments for capital mobilization and economic development.

Investment funds

Following the enactment of the Law for the Development of New Financial Instruments and Institutions in 2005, the establishment of exchange-related mutual funds in Iran became possible for the first time. The primary objective of this law was to enhance indirect public participation in the capital market and reduce investment risk. Within this regulatory framework, the first investment fund in Iran was launched in 2008. This fund was an open-ended equity fund, meaning its units were not traded on the stock exchange.

In 2010, the Iran Securities and Exchange Organization (SEO) issued the first licenses for the establishment of exchange-traded funds (ETFs) in Iran. The first ETFs allowed investors to trade fund units on the stock exchange, offering higher liquidity compared to traditional open-ended funds.

Following the 2005 law, various financial institutions gradually emerged, each aiming to launch different types of investment funds. This period also marked a transition from the traditional open-ended mutual fund model to the ETF model, aligning Iran with global ETF practices. By 2014, the number of active investment funds in Iran had grown from a few dozen to over 100, reflecting the rapid development and diversification of the industry.

Rapid growth (2019-present)

The advent of online subscription and redemption platforms, together with digital brokerage portals, has substantially facilitated public access to investment funds in Iran. In recent years, several new categories of funds have been introduced, including gold and various fixed-income ETFs, index funds, private equity funds, leveraged equity funds, sector-specific funds, real estate funds and pension funds.

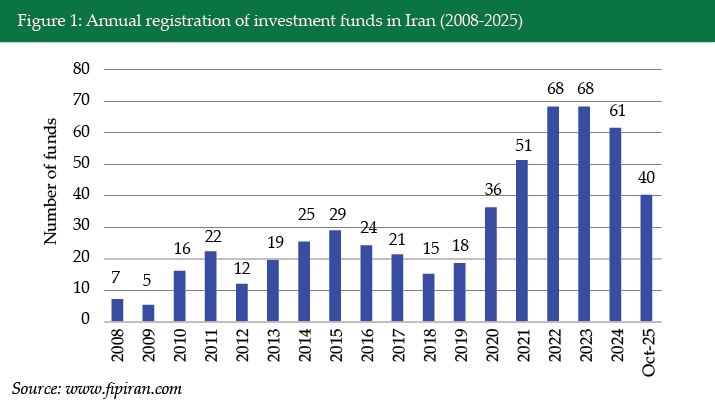

Since 2021, the participation of retail investors in these funds has increased markedly, positioning them as the principal instruments for mobilizing indirect liquidity within the Iranian stock market. Overall, both the number and diversity of investment funds in Iran have experienced rapid growth. The annual registration of investment funds from the inception of the market to the present is summarized in Figure 1.

How do they work?

In Iran, all types of investment funds are structured with a fund manager, a custodian and an auditor. Depending on the fund type, additional governing bodies may also be present. The fund manager is responsible for investment decisions and the overall execution of the fund’s strategy, while the custodian and auditor provide oversight to ensure proper management and compliance.

Iran hosts four main stock exchanges, and funds are typically listed on one of these exchanges according to their type. Exceptions include specialized market-making funds and retirement funds, which operate under an issuance and redemption framework and are therefore not listed on the exchanges. In addition, each of the stock exchanges, as well as the SEO, supervises the performance of the funds.

Fund statistics and data

Currently, as shown in Table 1, there are 16 types of investment funds in the Iranian capital market. The table also presents the number of funds in each category along with their total AUM.

| Table 1: Investments funds in Iranian capital market | |||

| No | Category | Number of funds | AuM (US$ million) |

| 1 | Fixed income funds | 164 | 10,120 |

| 2 | Market-making/proprietary funds | 117 | 2,446 |

| 3 | Commodity-backed securities funds | 28 | 1,981 |

| 4 | Equity funds | 118 | 635 |

| 5 | Leveraged equity funds | 9 | 565 |

| 6 | Sector equity funds | 25 | 519 |

| 7 | Balanced/mixed funds | 17 | 57 |

| 8 | Pension/retirement funds | 6 | 51 |

| 9 | Index equity funds | 7 | 36 |

| 10 | Real estate funds | 6 | 33 |

| 11 | Capital guaranteed funds | 5 | 33 |

| 12 | Project-based/infrastructure funds | 1 | 25 |

| 13 | Private/private placement funds | 6 | 19 |

| 14 | Fund of funds | 5 | 19 |

| 15 | Venture capital funds | 19 | 5 |

| 16 | Real estate development/land and building funds | 4 | 2 |

| Total | 537 | 16,547 | |

| Source: www.fipiran.com | |||

Future strategies for investment funds

As Iran’s capital market continues to expand, the role and importance of investment funds are becoming increasingly significant. In recent years, the diversification of these funds has improved considerably; however, certain structural and product gaps persist within the sector. For instance, the Iranian market currently lacks hedge funds, international funds, growth funds, value funds and inflation-protected bond funds – all of which play crucial roles in more mature financial systems.

The managers of investment funds and their investment committees, through the specialized assessment of investment opportunities, contribute to enhancing allocative efficiency. The greater the diversity of fund types, the broader the range of sectors in which such efficiency can be observed. Moreover, venture capital and private equity funds, which typically invest in start-ups and small enterprises with high growth potential, play a significant role in promoting economic growth within societies.

The SEO of Iran, as the principal regulatory authority overseeing the approval and enforcement of capital market regulations, has outlined strategic plans to broaden both the range and the volume of investment funds available. Notably, commodity-backed securities funds based on assets such as gold and saffron have already been launched, and further initiatives are underway to introduce similar funds backed by silver, copper and other key commodities.

Conclusion and outlook

Over the past decade, Iran’s investment fund industry has undergone notable expansion and diversification, signaling the gradual evolution of the country’s capital market toward greater institutional maturity. Nevertheless, several structural and regulatory limitations continue to constrain its overall potential, particularly the lack of specialized investment vehicles and limited engagement with international financial systems.

Moving forward, sustained regulatory reforms, technological advancements and the introduction of innovative fund structures are expected to enhance market depth, strengthen investor confidence and foster a more resilient financial ecosystem. Effective supervision, coupled with transparent governance, will be essential to ensuring the sustainable development of this growing sector.

Furthermore, Iran represents a largely untapped and emerging market with considerable potential across various economic domains. The gradual easing of international restrictions could unlock significant opportunities for capital inflows and market expansion, particularly within the investment fund industry. Leveraging these opportunities could position Iran’s capital market as a dynamic regional hub for diversified investment and sustainable economic growth.

Hossein Jalilinia is the senior investment analyst at Iran Fara Bourse. He can be contacted at Hosseinjalilinia74@gmail.com.