- Institutional giants stand tall over fragmented retail-focused offerings

- Malaysia remains the global heavyweight, followed by Saudi Arabia

- Regulatory harmony and digital fintech can unlock Africa’s massive, untapped potential

Amid the prevailing tremors of the global markets, especially at the end of 2025, a disciplined corner of the financial world continued asserting its stabilizing influence: Shariah compliant equities.

Though still dismissed as a peripheral concern for a specialized clientele, these vehicles – governed by Islamic principles that eschew excessive debt and speculative risk – have increasingly emerged as a sturdy redoubt for investors navigating broader economic upheaval.

With the S&P 500 Shariah Index outperforming the base S&P 500 by 1% and 3% in 2024 and 2025 respectively, the appeal of Islamic equities has extended beyond capital preservation as they prove moral clarity can coexist with competitive vigor.

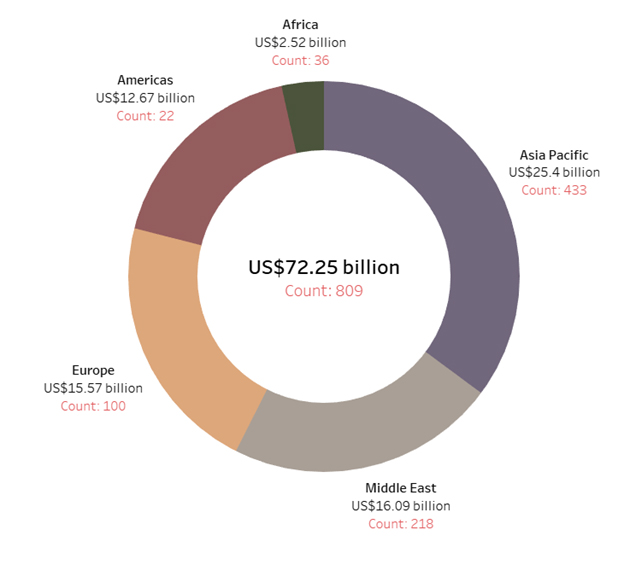

The growth, though, hasn’t been geographically even. Asia Pacific has the largest total AuM for equities, at just over US$25 billion, followed by the Middle East, Europe and the Americas, which have an average of nearly US$15 billion tracking for each region.

Performance-wise, traditional core Islamic markets in the Middle East have experienced a more muted growth profile. Despite being the historical heart of the industry, these markets are currently grappling with local fragmentation and a lack of large-scale, globally distributed products.

The challenge for these regions moving forward will be to consolidate their domestic offerings and create investment vehicles that can capture the burgeoning institutional demand on a global scale.

Dominance of the Asia Pacific region

The Asia Pacific region continues to be the primary engine of the global Shariah equities market, commanding US$25.4 billion in total AuM distributed across 433 funds tracked by the IFN Investor Funds Database.

This geographic stronghold owes its prominence to a sophisticated regulatory environment and an unusually high level of retail participation, largely anchored in the Muslim-majority hubs of Southeast Asia.

The region also had the highest global growth for Shariah equities, expanding 32% between Q3 and Q4 2025. However, beneath these headline figures lies a landscape defined by significant internal variation in fund scale and market maturity.

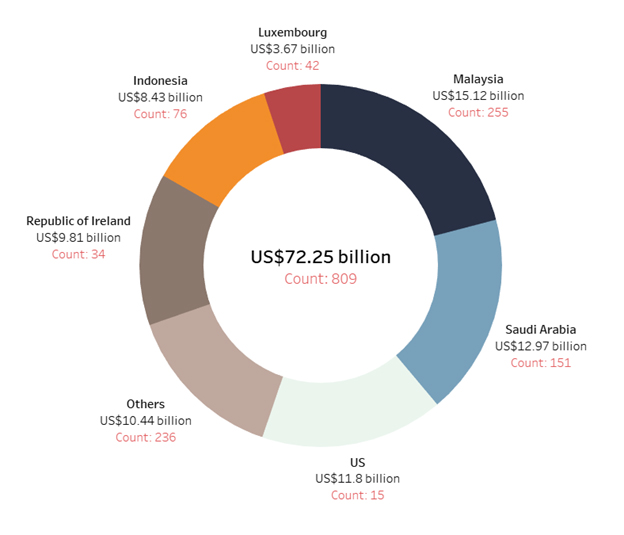

Malaysia remains the global heavyweight in this sector, serving as the domicile for 255 funds with a combined capitalization of US$15.12 billion. Its disproportionate influence is a direct result of decades of proactive government policy and the development of a comprehensive legal framework that has successfully institutionalized Islamic finance.

As the world’s most advanced Islamic investment market, Malaysia sets the benchmark for how domestic support can translate into global leadership.

In contrast, Indonesia presents a narrative of untapped potential and retail fragmentation. Despite housing the world’s largest Muslim population, its market is characterized by 76 funds managing a collective US$8.43 billion – figures that suggest a proliferation of smaller, localized products rather than the massive, consolidated vehicles seen in Western hubs.

While this high fund count indicates a vibrant and growing grassroots interest, it also highlights the ongoing challenge of achieving the economies of scale necessary for global institutional competition.

Chart 1: Shariah equity markets by region, AuM and fund count

Middle East: A stronghold formed by sovereign capital

The Middle East, long the geographical and cultural heart of Islamic finance, is also a powerhouse of Shariah compliant equities, commanding US$16.09 billion in assets across 218 individual funds.

Yet the region presents a structural paradox: while it possesses one of the world’s most deeply entrenched Islamic financial systems, its equity market is remarkably fragmented – split across a patchwork of national regulatory regimes from Riyadh to Abu Dhabi. The Middle East also experienced a decline of 8.3% in total AuM between Q3 and Q4 2025.

Saudi Arabia stands as the undisputed titan of the Gulf, hosting 151 funds with a total capitalization of US$12.97 billion. This dominance is largely a reflection of the Kingdom’s aggressive efforts to deepen its capital markets as part of broader economic reforms, catering to a vast domestic base of retail and corporate clients.

The primary engine behind the region’s massive asset pool, however, is not the individual saver but the institutional giant. Sovereign wealth funds in the Middle East have become the ultimate bulwark of the market, deploying large-scale allocations into Shariah compliant products.

Whether through internal mandates or by seeding local investment vehicles, these institutional behemoths provide the liquidity and stability that define the Middle Eastern market, even as various initiatives seek to navigate the complexities of local fragmentation.

Chart 2: Shariah equity markets by fund domicile

Table 1: Shariah equity funds ranked by quarter-on-quarter AuM growth

| Region | Q3 2025 (US$ billion) | Q4 2025 (US$ billion) | AuM change (%) |

| Africa | 2.38 | 2.52 | 6.07% |

| Americas | 13.44 | 12.67 | -5.71% |

| Asia Pacific | 19.24 | 25.4 | 32.04% |

| Europe | 14.04 | 15.57 | 10.88% |

| Middle East | 17.55 | 16.09 | -8.31% |

Europe: Institutional gateway to global capital

Europe maintains its standing as the world’s third-largest hub for Shariah compliant equities, commanding US$15.57 billion in total AuM. Yet, in a stark departure from the retail-heavy markets of Asia, Europe achieves this scale through a remarkably lean structure of just 100 funds.

This footprint – nearly half the fund count of the Middle East – underscores Europe's specialized role not as a local retail market. It also remains as a sophisticated global gateway for institutional capital, growing 10.88% in total AuM between Q3 and Q4 2025.

The Republic of Ireland has solidified its position as the premier European domicile for Islamic equities, hosting US$9.81 billion in assets across 34 funds. Along with Luxembourg and the UK, these jurisdictions serve as the preferred staging grounds for large-scale, globally distributed investment vehicles.

The efficiency of the European model is driven by a unique dual dynamic. Major financial institutions from both the Middle East and Asia frequently utilize European hubs to domiciliate funds that aggregate capital from a truly global investor base.

By leveraging the EU’s sophisticated regulatory framework, these managers can launch fewer, substantially larger funds that benefit from significant economies of scale, effectively siphoning capital from around the world into a concentrated pool of institutional-grade Shariah assets.

Americas: Institutional power

The Americas present a distinct model of market concentration, where institutional scale far outweighs the sheer number of active products. Despite having the smallest global fund count of 22 and a 5.71% deficit in AuM between Q3 and Q4 2025, the region commands the fourth-largest total capitalization at US$12.67 billion.

This profile represents the most dramatic instance of high-capitalization density: with an average of roughly US$576 million per fund, the Americas boast the highest average AuM per vehicle in the world. This structural lean toward a few, massive institutional vehicles is a defining characteristic of the North American landscape.

Shariah compliant funds in this region largely cater to the growing demand for passive and index-tracking strategies. The US market, in particular, has become a hub for high-volume, low-cost ETFs and mutual funds that mirror benchmark indices like the S&P 500 Shariah or the MSCI World Islamic Index.

By pooling vast amounts of capital into single, streamlined legal structures, these products attract the world's most significant institutional players. Sovereign wealth funds, university endowments and large-scale pension funds increasingly favor these vehicles, often allocating capital in multi-billion-dollar tranches.

This institutional gravity has turned the Americas into a formidable pillar of the global Shariah equities market, characterized by efficiency and deep liquidity rather than regional fragmentation.

Africa: Untapped frontier of retail growth

Africa presents a compelling study in market potential, characterized by a vibrant but localized landscape of Shariah compliant equities. Despite maintaining a significantly higher fund count than the Americas – at 36 individual funds – the region’s total capitalization stands at US$2.52 billion.

This modest figure, representing only 20% of the American total, highlights a market defined by high volume and low average AuM, typically averaging around US$70 million per vehicle. Africa also experienced a 6% sectoral growth in Shariah equity AuM between Q3 and Q4 2025.

This structural divergence is driven by the highly specific, fragmented nature of the African investment landscape. Unlike the institutional, passive-dominated models of the West, African funds are often designed to serve a diverse array of local retail savers and high-net-worth individuals.

These vehicles must navigate a complex patchwork of cultural demands and evolving legal frameworks across nations like Nigeria, Kenya and Morocco, necessitating a larger number of smaller, more focused products.

The nascent status of many African markets further compounds this fragmentation. As younger funds struggle to reach the critical mass seen in more mature jurisdictions, they remain focused on domestic equities and local liquidity.

However, as regulatory structures begin to harmonize and digital fintech solutions bridge the gap to unbanked populations, Africa is positioned as the next major growth frontier for global Shariah compliant capital.

The largest Shariah equity funds

The HSBC UCITS Common Contractual Fund (CCF) – Islamic Global Equity Index Fund, specifically the A2CGBP share class, stands as a behemoth in the Shariah compliant equity space, representing the institutional gravity that now defines the Western market. Domiciled in Ireland, this fund is a primary example of how large-scale, low-cost vehicles are aggregating global capital into a singular, transparent structure.

Table 2: Shariah equity funds ranked by AuM

| Rank | Fund name | Fund company | AuM (US$ million) |

| 1 | HSBC UCITS Common Contractual Fund - Islamic Global Equity Index Fund - Class A2CGBP | HSBC Asset Management | 4,758.76 |

| 2 | Amana Growth Institutional Fund | Saturna Capital | 3,280 |

| 3 | Amana Growth Investor Fund | Saturna Capital | 2,730 |

| 4 | Bahana USD Global Sharia Equities | Bahana TCW Investment Management | 2,460.32 |

| 5 | SP Funds S&P 500 Sharia Industry Exclusions ETF | ShariaPortfolio | 1,969.97 |

| 6 | Bahana US Opportunity Sharia Equity USD | Bahana TCW Investment Management | 1,886.44 |

| 7 | Mandiri Asia Sharia Equity Dollar (Kelas A) | Mandiri Manajemen Investasi | 1,600 |

| 8 | Amana Income Institutional Fund | Saturna Capital | 1,310 |

| 9 | Albilad CSOP MSCI Hong Kong China Equity ETF | Albilad Capital | 1,309.27 |

| 10 | Public Asia Ittikal Fund | Public Mutual | 1,113.84 |

Top-performing Shariah equity funds

Leading the pack of top-performing Shariah funds is the Pacific Saham Syariah III, an Indonesian-domiciled equity fund that is managed by PT Pacific Capital Investment.

At the end of Q4 2025, Pacific Saham Syariah III’s three-month return of 68.47% significantly outpaced global Shariah benchmarks and conventional indices alike.

Table 3: Islamic equity funds ranked by three-months returns

| Rank | Fund name | Fund company | Three-month returns (%) |

| 1 | Pacific Saham Syariah III | Pacific Capital Investment | 68.47 |

| 2 | Capital Sharia Equity | Capital Asset Management | 49.62 |

| 3 | Re-Pie Portfolio Management Participation Mixed Venture Capital Investment Fund | Re-Pie Portfoy | 44.35 |

| 4 | Pratama Syariah | Pratama Capital Assets Management | 43.63 |

| 5 | Narada Saham Berkah Syariah | Narada Asset Management | 42.52 |

| 6 | Minna Padi Indraprastha Saham Syariah | Minna Padi Aset Manajemen | 36.82 |

| 7 | Nomura Global Shariah Semiconductor Equity Fund - USD Class | Nomura Asset Management Malaysia | 35.89 |

| 8 | Nomura Global Shariah Semiconductor Equity Fund- MYR Class | Nomura Asset Management Malaysia | 32.93 |

| 9 | Sucorinvest Sharia Equity Fund | Sucorinvest Asset Management | 31.31 |

| 10 | Aurora Sharia Equity | Aurora Asset Management | 24.61 |

Outlook

While the Asia Pacific region remains the primary engine for retail engagement and fund volume, the explosive growth in the Americas and Europe signals a definitive shift toward massive, passive investment structures.

The ability of core Islamic markets in the Middle East and Southeast Asia to scale their domestic products into globally distributed vehicles will be essential to capturing the next wave of institutional capital.

Moving forward, the harmonization of regulatory standards and the rise of digital fintech solutions – particularly in nascent frontiers like Africa – are poised to bridge the gap between fragmented local markets and global liquidity.

Ultimately, the increasing integration of Shariah compliant equities into mainstream portfolios suggests that this once-niche sector is now becoming an indispensable pillar of the global financial architecture.

Restricted Access

Login to continue reading (existing subscriber)

Subscribe NOW and get:

- Gain unlimited access through all key operating platforms

- Full access to all listed Islamic funds & fund profiles

- Unlimited access to all Islamic fund managers

- Access to all exclusive articles, reports, podcasts & videos

- Complimentary access to all IFN Investor Forums