- Shariah equities outperformed global benchmarks in Q3 2025

- Americas and Europe saw explosive AuM growth; Middle East lagged

- Global market is highly diverse, led by Asia Pacific funds in count

In an era defined by global financial volatility, a quiet but powerful force in the investment landscape continues to prove its mettle: Shariah compliant equities.

Once relegated to a niche sector, the market guided by the moral precepts of Islam has repeatedly shone during periods of financial turmoil, transforming these funds into a perceived "safe haven" for investors.

While ethical screening provides a compelling buffer against speculative excesses, the defensive resilience has not come at the expense of performance. Shariah equities have provided returns commensurate with key global indices, delivering risk-adjusted returns that stand toe-to-toe with their conventional benchmarks.

In the third quarter of 2025, the S&P Global BMI Shariah index gained 8.9%, slightly outperforming the conventional S&P Global BMI, which rose by 7.8%. The S&P 500 Shariah Index, tracking compliant US stocks, demonstrated even stronger short-term leadership, rising by 10.2% in Q3 2025, significantly outpacing the 8.1% gain of the benchmark S&P 500.

Over the full one-year horizon, performance remains highly comparable, with the S&P 500 Shariah and the S&P 500 posting nearly identical total returns (17.4% and 17.6%, respectively). This data strongly affirms the argument that adherence to ethical principles does not compromise an investor's ability to capture global market gains.

A diverse and expanding global footprint

The Islamic equities market is far from monolithic. The world’s top Shariah compliant companies alone boasted a combined market capitalization exceeding US$16.9 trillion as of 2025, underscoring their massive influence in the global economy.

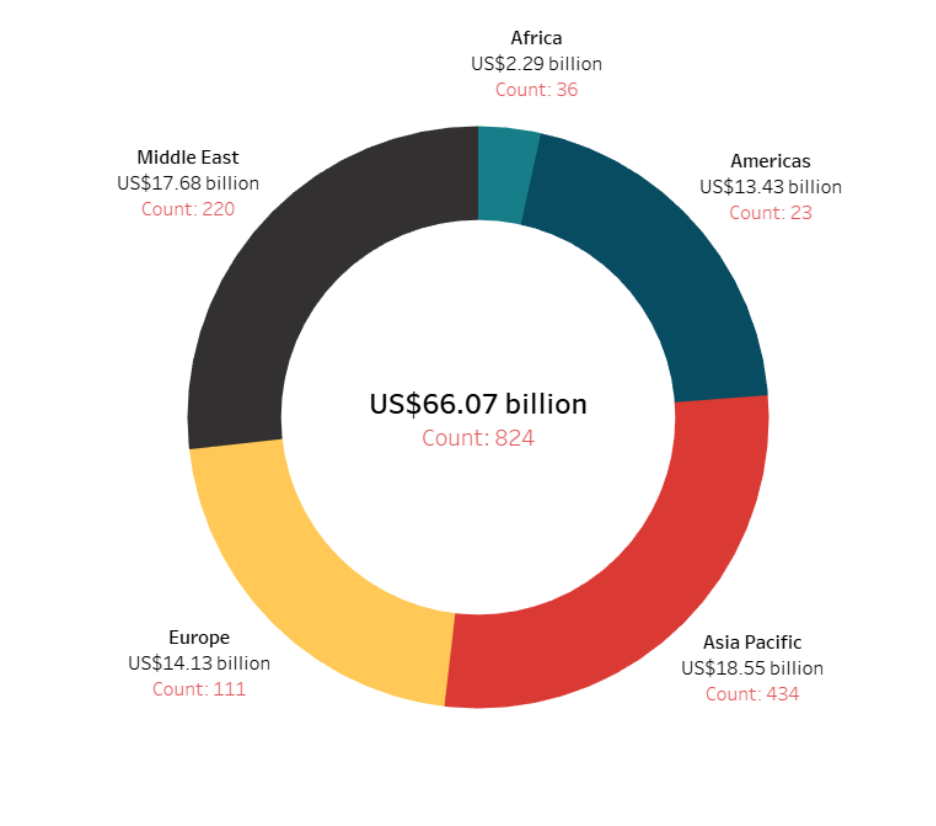

The IFN Investor Funds Database reveals the global Shariah equities market as a dynamic and geographically diverse industry, anchored by regional heavyweights but characterized by significant disparities in fund structure and scale. The overall market, captured in the chart, represents a total of 824 funds globally with a combined AuM of US$66.07 billion.

The largest Shariah compliant firms, often technology and energy giants, are headquartered across the US, Saudi Arabia and East Asia, confirming that this once-niche sector is now deeply integrated into the world's most valuable industries.

Chart 1: Shariah equities funds by region, fund count and AuM

Asia Pacific: The fragmented chart-topper

The Asia Pacific region is the indisputable market leader for Shariah equities, topping both AuM at US$18.55 billion and fund count at 434. It stands out primarily due to its high level of regulatory maturity and deep retail engagement, driven by its large Muslim-majority population in Southeast Asia.

In Asia, Malaysia hosts the highest number of funds globally at 259. With US$14.5 billion in AuM and being a core driver, it is benefiting from sustained government support and an advanced framework that has positioned it as the world's leading Islamic investment market.

Indonesia is a distant second in this region, with US$2.26 billion in capitalization and 79 funds in count. While it has the world's largest Muslim population, the high fund count paired with moderate capitalization indicates a rapidly growing but highly fragmented domestic retail market that is still developing the scale of its funds.

The Asia Pacific's highly fragmented, retail-driven Shariah market has 19 times the number of Islamic equity funds as the Americas – the smallest of the regions – but only a marginal US$5 billion more in total AuM.

Middle East: A bulwark of sovereign wealth funds

The Middle East, home to the largest Islamic finance system globally, commands the second-highest AuM at US$17.68 billion across 220 funds that also reflect a fragmented yet deeply entrenched market.

While the total AuM is massive, the fund count is high because the region encompasses several distinct nations – including Saudi Arabia, UAE and Qatar – each with its own regulatory regime and a large number of local financial institutions offering funds to a vast retail and domestic business client base. Saudi Arabia leads the GCC in both capitalization and fund count, at US$14.72 billion and 148, respectively.

The Middle East’s high AuM is primarily driven by the region's enormous capital pool, particularly from sovereign wealth funds. These institutional giants often dedicate significant, large-scale allocations to Shariah compliant products, either through internal mandates or by seeding local funds.

Europe: The international domicile and gateway

Europe ranks third in AuM at US$14.13 billion but has nearly half the fund count of the Middle East, with 111 funds. This structural difference highlights Europe's role as a sophisticated financial hub. Europe's market is a clear case of lower fund count yielding a higher average fund capitalization compared to the Middle East.

Ireland is Europe’s leading domicile for Shariah equities with AuM of US$9.11 billion and 34 funds.

European jurisdictions, particularly Luxembourg and the UK, are not primarily markets for local retail Islamic investment – but rather serve as crucial domiciles for globally distributed funds. Luxembourg, for instance, is the leading center outside the Muslim world for Islamic funds by number of funds established.

The funds domiciled in Europe are often large, "umbrella" or UCITS-compliant structures used by major international asset managers including those from the Middle East and Asia, to raise capital from European and global investors.

The regulatory sophistication and investor protection inherent in the EU framework – especially for UCITS – make these structures appealing for large, institutional and high-net-worth investors, naturally resulting in fewer, but substantially larger funds.

Essentially, Europe houses vehicles that gather capital from global investors including the capital generated in the Middle East, leading to a high AuM value concentrated in a smaller number of funds.

The institutional power of the Americas

Despite ranking last in fund count with just 23 funds, the Americas still commands the fourth-largest total capitalization at US$13.43 billion. This is the clearest example of high capitalization with low fund count, resulting in the highest average AuM per fund globally. The structure is a strong indicator of a market dominated by a few, very large institutional investment vehicles. Shariah compliant funds in the Americas often cater to passive and index-tracking products.

The US market, in particular, favors large, low-cost ETFs and mutual funds that track major Shariah compliant indices like the S&P 500 Shariah or MSCI World Islamic Index. These products pool massive capital into single legal structures. They are taken up by large-scale institutional investors such as sovereign wealth funds, university endowments or large pension funds that allocate capital in multi-billion-dollar tranches to a limited number of fund managers.

Africa: Underdeveloped and full of potential

Africa has far more funds (36) than the Americas (23), yet its total AuM is only US$2.29 billion – a mere 17% of the American total. Here, funds are often created to serve highly specific, local investor bases across different countries – think Africa (excluding North Africa). They tend to be smaller, focused on domestic Shariah compliant equities and primarily geared toward retail savers and high-net-worth individuals, which require more vehicles to serve diverse legal and cultural demands.

Also, nascent markets, such as in parts of Africa, often feature smaller, younger funds that have not yet achieved the scale of their global counterparts. Regulatory structures across different nations can also require a proliferation of distinct, small funds, limiting the ability of managers to consolidate and reach a critical mass of capitalization.

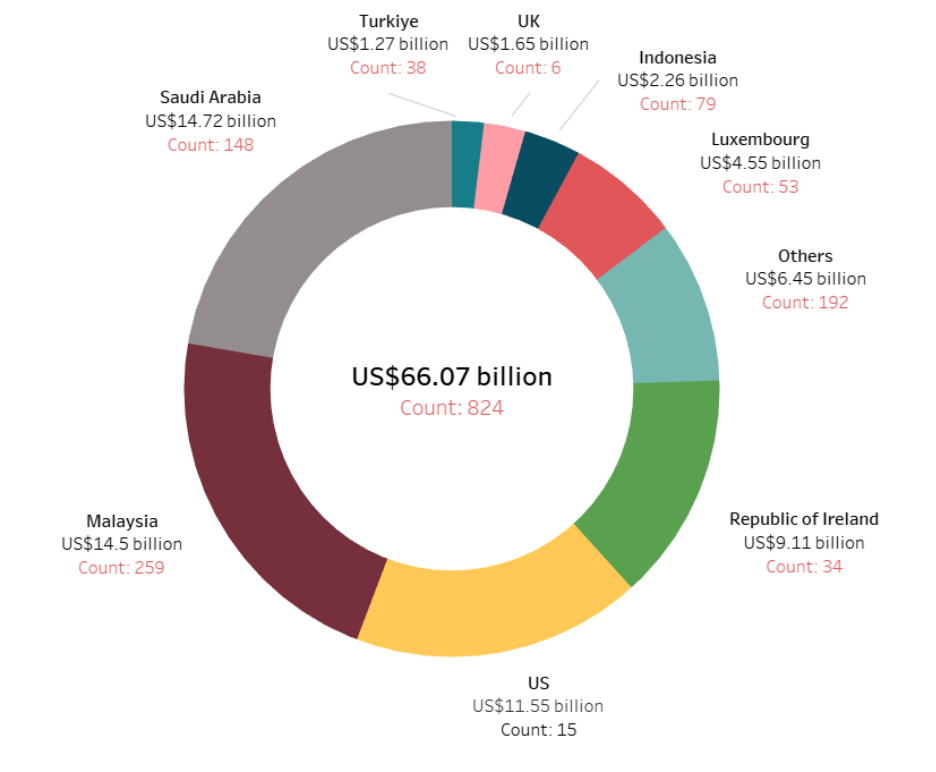

Chart 2: Shariah equity market by domicile, fund count and AuM

Anglo-Asian bank HSBC’s Irish-domiciled HSBC UCITS Common Contractual Fund is the world’s largest Shariah compliant equity fund, with an AuM of US$4.62 billion.

Other funds in the top five include two US-based Amana Growth funds, with AuM of US$3.33 billion and US$2.75 billion, respectively; US-domiciled ShariaPortfolio’s SP Funds at US$1.81 billion and Saudi-based Albilad Capital’s US$1.55 billion Albilad ETF.

Among the top performing five funds, the first three spots were secured by China-focused funds, which benefited from a sharp rally in China A-shares. They are Malaysian-based RHB Asset Management’s USD- and RM-denominated funds, which returned 46.02% and 45.97% in the three months to September 2025.

Q3 2025 also saw a highly divergent pattern in Shariah equities AuM growth, with Western financial hubs significantly outpacing the core markets of the Middle East. The Americas and Europe led the charge with quarterly growth averaging in excess of 13%.

Table 1: Largest equity funds globally

| Rank | Fund | Manager | AuM (US$ million) |

| 1 | HSBC UCITS Common Contractual Fund - Islamic Global Equity Index Fund - Class A2CGBP | HSBC Asset Management | 4,624.37 |

| 2 | Amana Growth Institutional Fund | Saturna Capital | 3,330 |

| 3 | Amana Growth Investor Fund | Saturna Capital | 2,750 |

| 4 | SP Funds S&P 500 Sharia Industry Exclusions ETF | ShariaPortfolio | 1,809.95 |

| 5 | Albilad CSOP MSCI Hong Kong China Equity ETF | Albilad Capital | 1,550.05 |

| 6 | Amana Income Institutional Fund | Saturna Capital | 1,270 |

| 7 | Bahana Global Healthcare Sharia USD Equity Fund | Bahana TCW Investment Management | 1,060.59 |

| 8 | Invesco Dow Jones Islamic Global Developed Markets UCITS ETF Acc | Invesco Capital Management | 1,051.98 |

| 9 | Public Ittikal Sequel Fund | Public Mutual | 1,049.36 |

| 10 | Public Asia Ittikal Fund | Public Mutual | 1,045.41 |

Chart 2: Top performing equities funds

| Rank | Fund Name | Fund Manager | Three-months return (%) |

| 1 | RHB Shariah China Focus Fund - USD | RHB Asset Management | 46.02 |

| 2 | RHB Shariah China Focus Fund - RM | RHB Asset Management | 45.97 |

| 3 | VP-DJ Shariah China A-Shares 100 ETF | Value Partners Asset Management | 36.84 |

| 4 | KSE Meezan Index Fund | Al Meezan Investment Management | 32.94 |

| 5 | Mahaana Islamic Index ETF | Mahaana | 30.39 |

Table 3: Regional equities growth

| Region | AuM Q2 2025 (US$ million) | AuM Q3 2025 (US$ million) | Change (%) |

| Africa | 2,163.97 | 2,295.76 | 6.09% |

| Americas | 11,729.4 | 13,428.2 | 14.48% |

| Asia Pacific | 16,527.52 | 18,558.19 | 12.29% |

| Europe | 12,480.42 | 14,134.13 | 13.25% |

| Middle East | 17,465.54 | 17,668.58 | 1.16% |

Outlook

The robust Q3 2025 performance reaffirms that Shariah screening provides both ethical alignment and competitive returns, often benefiting from its inherent quality bias and exclusion of highly leveraged sectors.

The significant growth disparity between regions highlights a structural trend where global capital including Middle Eastern sovereign wealth, is increasingly flowing into large, institutional ETF and UCITS structures domiciled in Western financial hubs.

For core Islamic markets in the Middle East and Asia Pacific, the key challenge moving forward is to overcome local fragmentation and scale domestic funds into globally distributed products to capture this institutional demand.

Consequently, the future of the US$66 billion market will be defined by a dual dynamic: continued retail depth across Asia, coupled with the explosive institutional growth driven by passive and index-tracking strategies globally.

Restricted Access

Login to continue reading (existing subscriber)

Subscribe NOW and get:

- Gain unlimited access through all key operating platforms

- Full access to all listed Islamic funds & fund profiles

- Unlimited access to all Islamic fund managers

- Access to all exclusive articles, reports, podcasts & videos

- Complimentary access to all IFN Investor Forums