Despite the UAE being arguably the worst hit in the GCC from Iran’s retaliation to the US-Israeli attack, institutional players still see its overall economy as resilient – amid pockets of concern.

“Economic growth in this region is actual and stable. I’m talking about growth in real terms, after considering inflationary factors, unlike nominal numbers in the US or Europe,” Nahda Capital Partners Founding CEO Inigo de Luna shared with IFN Investor.

He said that Nahda Capital is still launching its fund in April 2026 to focus on the SME sector, where there is a high percentage – around 85% – of companies being family-owned and facing generational transfer hurdles.

Though concerns remain on how long the conflict will continue, Inigo said: “Yes, there's a bump right now. It's a crisis. But we are in Dubai doing business as usual. Returns for a PE fund will take around 10 years. What is three to four weeks of uncertainty, when compared to 10 years?”

However, the UAE’s real estate could suffer, due to its large expatriate population. “The allure of Dubai may be under threat at the moment, but S&P Global Ratings doesn't expect a 2008-style property crash in Dubai if the intense phase of conflict lasts up to four weeks.”

Anticipating a surge in secondary market transactions with price declines as investors try to offload their properties, the firm projected the worst hit would be the luxury and ultra-luxury segment – especially among foreigners who moved to the UAE for tax or lifestyle reasons.

While some properties have been impacted, the ratings firm said the damage until now has not been to a degree beyond repair. “If developers have war risk insurance, then the damage can be covered.”

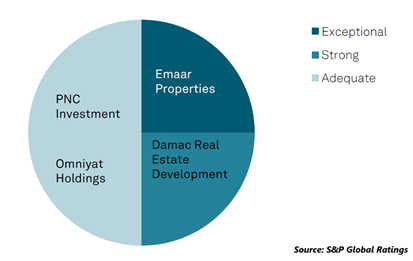

Chart 1: Liquidity assessment for rated Dubai developers

S&P Global Ratings noted that Damac Real Estate Development and Omniyat Holdings issued US$600 million Sukuk in February 2026 and March 2026 respectively, while PNC Investment and Omniyat Holdings issued US$1.25 billion and US$900 million respectively in 2025. “Debt maturities remain quite manageable in 2026 for the companies without the need to raise new funding.”

Meanwhile, Fitch Ratings noted that new US dollar Sukuk issuances from GCC issuers have fallen significantly since the start of the Iran war. “While some yield widening is visible in GCC bonds and Sukuk since the war began, there have not been market wide sell-offs. Despite heightened geopolitical challenges in recent years, GCC issuer activity rebounded quickly once tensions eased.”

Restricted Access

Login to continue reading (existing subscriber)

Subscribe NOW and get:

- Gain unlimited access through all key operating platforms

- Full access to all listed Islamic funds & fund profiles

- Unlimited access to all Islamic fund managers

- Access to all exclusive articles, reports, podcasts & videos

- Complimentary access to all IFN Investor Forums