UAE: A two-speed Shariah engine anchored by property, fueled by equities

- Bulk of fund AuM anchored in four massive real estate trusts

- Retail investors push equities as the market’s most popular fund choice

- Global ETFs, led by China and Turkiye, drive recent top performance

In the bustling financial corridors of the UAE, the Islamic funds industry tells a tale of two distinct markets. A monolithic real estate sector commands the lion’s share of capital – its unmistakable presence like the Burj Khalifa, the world's tallest building. The other is a vibrant but fragmented collection of equity and debt funds vying for the attention of a growing class of ethical investors.

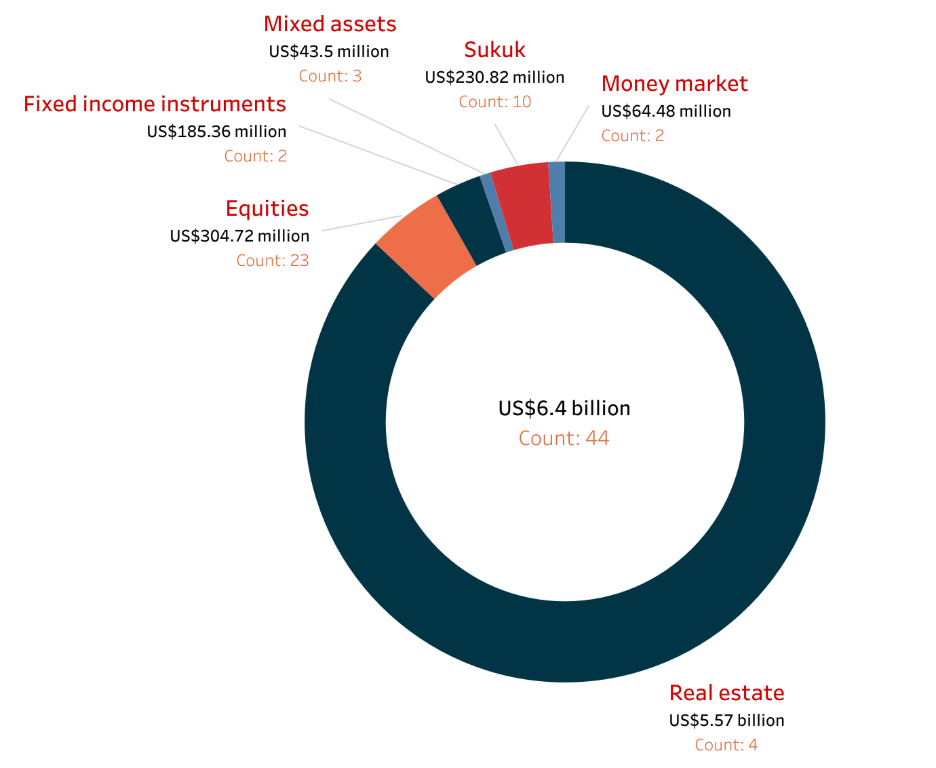

As of Q3 2025, the UAE’s Shariah compliant funds industry oversaw roughly US$6.4 billion in assets across 44 funds tracked by the IFN Investor Funds Database. Yet, a look beneath the headline numbers reveals a landscape defined by extreme concentration.

The narrative is dominated by bricks and mortar, where real estate funds hold a staggering US$5.57 billion – roughly 87% of the entire industry’s assets – despite comprising only four actual funds. Of these, the Dubai Residential REIT alone holds over US$4 billion in AuM.

This concentration reflects the "institutionalization" of the property market. With the UAE’s residential real estate market projected to hit multi-billion valuations in recent years, such capital has flooded into large-scale vehicles rather than scattered retail bets.

Institutional investors and family offices in the region have maintained real estate allocations significantly higher than the global average, often treating these funds as stable, long-term anchors for their portfolios.

Regulatory clarity has further greased these wheels. In early 2025, the Ministry of Finance clarified tax rules for REITs, reducing compliance burdens and likely encouraging foreign capital to park itself in these massive, Shariah compliant property vehicles.

Regional narrative

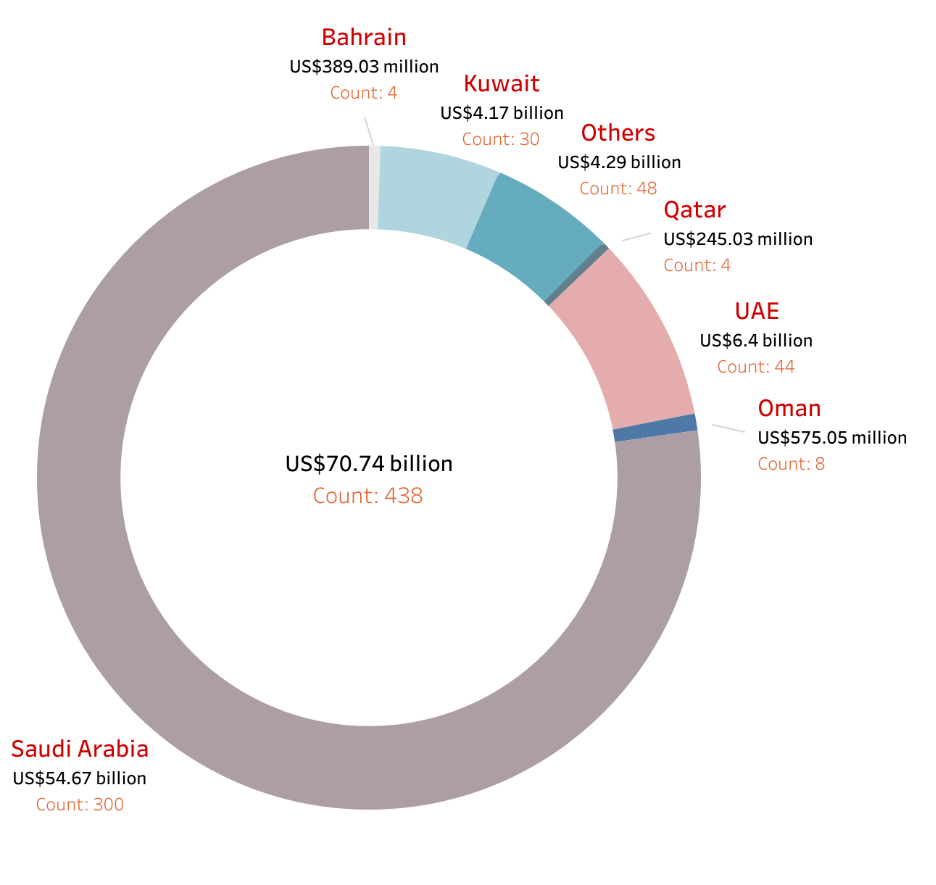

The UAE story is, of course, part of a broader regional narrative encompassing the GCC, a vast ecosystem of Middle East wealth with 438 public funds valued at US$70.74 billion tracked by the IFN Investor Funds Database.

Saudi Arabia dominates this extended market, with 300 funds worth US$54.67 billion. The UAE ranks second in the region, outpacing Kuwait (US$4.17 billion, 30 funds), Oman (US$575.05 million, eight funds), Bahrain (US$389.03 million, four funds) and Qatar (US$245.03 million, four funds).

Offerings with multiple domiciles make up a cumulative holding of US$4.29 billion across 48 funds.

Chart 1: GCC Shariah markets by domicile, AuM and fund count

The crowd favorite: Equities

While real estate holds the bulk of UAE cash values, equities hold the crowd. There are 23 Shariah compliant equity funds currently active – more than any other asset class – yet they manage a comparatively modest US$304.72 million.

This divergence highlights a shift in who is investing. While sovereign wealth funds back billion-dollar real estate projects, individual investors are increasingly turning to equity funds as accessible entry points into the market. The surge in fund count tracks with a broader deepening of the UAE’s capital markets, where a steady stream of IPOs from non-government entities and tech firms has provided new feedstock for these portfolios.

Yield hunters: Sukuk and fixed income

The debt market occupies the middle ground, led by Sukuk. With US$230.82 million across 10 funds, Sukuk remains the preferred vehicle for fixed-income investors over the alternate fixed income instruments segment, which holds just US$185.36 million.

This segment is currently undergoing a democratization moment, as 2025 marked a turning point where the UAE government opened Islamic treasury Sukuk to individual investors for the first time, allowing residents to invest with as little as AED4,000 (US$1,090). This policy shift suggests a growing appetite for Shariah compliant stable yield products that is likely to drive future growth in this asset class.

Niche alternative: Fixed income instruments

Trailing the more established Sukuk market, fixed income instruments hold a modest US$185.36 million across just two funds. This category is distinct from Sukuk, representing a niche segment likely focused on specialized Shariah compliant debt structures that go beyond traditional Islamic bonds. These might include funds investing in Murabahah, Ijarah or Istisna where the underlying assets or services provide a fixed, Shariah compliant return.

While Sukuk benefit from broad government issuance and a well-developed secondary market, these fixed income instruments often cater to highly specific institutional mandates or sophisticated investors looking for diversified Shariah compliant yield sources.

Their smaller footprint suggests they target less liquid, often private, transactions or more complex structures that require deeper due diligence than mainstream Sukuk offerings. The very limited number of funds also indicates a highly specialized expertise is required to manage these unique portfolios effectively, serving a select group of investors seeking alternatives to conventional fixed-income products.

Liquidity pool: Money market funds

With US$64.5 million spread across two funds, these funds are designed for capital preservation and immediate access to cash, typically investing in short-term, highly liquid Shariah-approved instruments such as short-term Murabahah deposits, commodity Murabahah or other cash management tools.

The modest AuM in this category reflects its primary role as a temporary parking spot for funds rather than a significant growth driver. Investors utilize money market funds to manage short-term cash flows, as a holding pen before deployment into longer-term investments, or as a low-risk option during periods of market uncertainty.

The presence of two funds indicates that both institutional and potential retail investors have access to Shariah compliant options for managing their working capital and ensuring liquidity while adhering to Islamic finance principles. This segment often thrives in environments with stable interbank rates and robust banking sector liquidity, providing a secure and accessible option for managing uninvested capital.

The hybrid: Mixed assets funds

At the back end with US$43.5 million across three funds, the mixed assets category offers diversified portfolios by combining various asset classes – typically a mix of equities, Sukuk and potentially real estate or money market instruments – within a single fund structure.

Despite the inherent appeal of diversification, the relatively small size of this segment suggests that investors in the UAE's Shariah space currently prefer pure-play strategies. This could be due to several factors: investors might prefer to build their own diversified portfolios with individual single-asset funds, or perhaps the existing mixed-asset offerings haven't yet resonated strongly enough with their risk-return profiles.

However, mixed-asset funds can be particularly attractive to retail investors or those seeking a 'one-stop-shop' solution for Shariah compliant investing – outsourcing asset allocation decisions to fund managers.

As the market matures and investor sophistication grows, there is potential for this segment to expand, particularly if funds can demonstrate superior risk-adjusted returns through dynamic asset allocation strategies tailored to the unique opportunities within the Islamic finance landscape. The current standing indicates a nascent stage, with room for growth as more sophisticated hybrid strategies emerge to meet diverse investor needs.

Chart 2: UAE Shariah funds by asset class and AuM as of Q3 2025

Fund performance

The largest three of the UAE’s Shariah funds are REITs, underscoring the dominance of bricks and mortar in its finance landscape.

DHAM REIT Management leads the pack with the US$4.39 billion Dubai Residential REIT, followed by Equitativa Group’ Emirates REIT (US$886 million) and Emirates NBD Asset Management’s ENBD REIT (US$236.6 million). Together, they account for US$5.51 billion – or 99% of the entire Shariah real estate holdings of the UAE, as tracked by the IFN Investor Funds Database.

Next to the property heavyweights were the Sukuk-focused Arqaam Islamic Income Fund (US$105 million), SHUAA Global Sukuk Fund (US$102.6 million) and the Target 2024 Sukuk Fund Series II (US$80.36 million).

The SHUAA Global Equity Fund led the equities category with an AuM of US$63.1 million, while The Sky One Money Market Fund with US$54.19 million, represented the money market sector.

Table 1: UAE’s largest capitalized Shariah funds

| Rank | Fund | Manager | AuM (US$ million) |

| 1 | Dubai Residential REIT | DHAM REIT Management | 4,389.48 |

| 2 | Emirates REIT | Equitativa Group | 886 |

| 3 | ENBD REIT | Emirates NBD Asset Management | 236.6 |

| 4 | Arqaam Islamic Income Fund | Arqaam Capital | 105 |

| 5 | SHUAA Global Sukuk Fund | SHUAA Capital | 102.6 |

| 6 | Target 2024 Sukuk Fund Series II | Azimut DIFC | 80.36 |

| 7 | Mashreq Al Islami Income Fund | Mashreq Capital | 64.9 |

| 8 | SHUAA Global Equity Fund | SHUAA Capital | 63.1 |

| 9 | Global Sharia REITS Portfolio | Invesense Asset Management | 55.83 |

| 10 | Sky One Money Market Fund | Al Ramz Asset Management | 54.19 |

Top returning funds

While real estate dominated in sheer asset size, the trailblazers for Q3 2025 Shariah performance in the UAE were a new wave of globally focused ETFs and specialized income funds.

Three of the top returning funds in this category belonged to one manager – Lunate Capital – which focused on high-growth markets like China, Hong Kong, Turkiye and the US to deliver an average return of more than 16% for its Chimera S&P group of funds.

Topping the table was the Chimera China HK Shariah ETF, which returned 19.53% in the three months to September 2025. The Chimera Turkiye Shariah ETF followed closely with a return of 19.38%. The US Shariah Growth ETF was third with 12.33%.

The high rankings of the Chimera S&P ETFs, along with the Aditum Islamic Income and Growth Fund in fourth spot, suggest that investors are increasingly looking at diversity and beyond local markets – particularly in fast-moving global equity sectors – for Shariah compliant capital appreciation.

But the SHUAA Global Equity Fund’s appearance at the bottom of the list, however, reiterates the popularity of stocks as a vehicle for the average UAE Shariah investor.

Table 2: UAE’s top returning Shariah funds

| Rank | Fund | Manager | Three-month return (%) |

| 1 | Chimera S&P China HK Shariah ETF - Income | Lunate Capital | 19.53 |

| 2 | Chimera S&P Turkiye Shariah ETF - Income | Lunate Capital | 19.38 |

| 3 | Chimera S&P US Shariah Growth ETF - Accumulating | Lunate Capital | 12.33 |

| 4 | Aditum Islamic Income and Growth Fund Open Ended IC Plc | Aditum Investment Management | 11.01 |

| 5 | SHUAA Global Equity Fund | SHUAA Capital | 9.9 |

Outlook

The UAE Shariah market will remain a tale of two sectors: Real estate as the institutional anchor and equities as the retail growth engine.

Real estate's stability, underpinned by three dominant REITs and favorable regulations, will attract slow, large-scale capital. Equity and other segments, while smaller, will drive fund proliferation as individual investors seek accessible entry points in a deepening capital market.

Future growth in the debt segment hinges on the democratization of yield. The government’s move to open Islamic treasury Sukuk to retail investors will spur demand for new Shariah compliant debt products. While Sukuk (US$230.82 million) leads the debt segment, managers must develop more sophisticated fixed-income strategies beyond traditional bonds to meet this rising retail appetite for yield and liquidity.

Performance investing is decisively moving beyond local markets too; the outperformance of Chimera S&P ETFs providing proof of this trend.

The current high concentration suggests near-term consolidation among non-real estate funds. The path to a more balanced market lies in attracting capital to the underrepresented segments – particularly by developing innovative mixed-asset solutions (US$43.5 million) that appeal to both institutional diversification needs and retail 'one-stop-shop' demands. The long-term trajectory depends on successfully integrating global performance vehicles with localized liquidity and stable property anchors.

Restricted Access

Login to continue reading (existing subscriber)

Subscribe NOW and get:

- Gain unlimited access through all key operating platforms

- Full access to all listed Islamic funds & fund profiles

- Unlimited access to all Islamic fund managers

- Access to all exclusive articles, reports, podcasts & videos

- Complimentary access to all IFN Investor Forums