Shifting sands of Shariah real estate: Asia Pacific gains as GCC slips

- Middle East the only region to experience q-o-q contraction

- Malaysia's flagship KLCC REIT surges to top of global capitalization ranking

- Turkish investment funds dominate performance with smaller returns

The shifting sands of global real estate are testing the traditional dominance of Middle Eastern capital hubs.

Q1 2026 global data shows the Middle East as the only region where quarter-on-quarter (q-o-q) valuations for real estate shrank. Growth was, meanwhile, registered in all the other Shariah hubs for real estate – from Africa to the Americas, Asia Pacific and Europe.

This suggests that the unprecedented geopolitical backdrop from the Middle East conflict had prodded some institutional investors at least to evaluate portfolio vulnerabilities in the GCC and apportion funds to safe-haven destinations away from the region.

Shift in global asset concentration

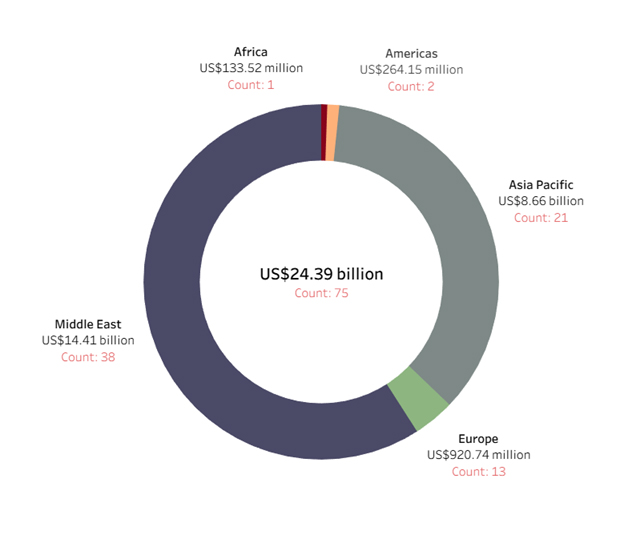

Global Shariah real estate funds remain largely stagnant at a rounded-up US$24.39 billion in Q1 2026, about 1.8% lower from the US$24.82 billion in Q4 2025.

The geographical distribution of public Shariah real estate vehicles appears to be undergoing a clear transformation. The macro compression was primarily driven by a visible retreat in the Middle East, where AuM dropped 5.57%, falling from US$15.26 million to US$14.41 billion.

Conversely, capital found a welcoming home in neighboring territories. The Asia Pacific market expanded its footprint by 3.62%, pushing its capital base up to US$8.66 billion.

Concurrently, smaller frontiers experienced aggressive inflows; Africa witnessed an explosive 220.53% q-o-q surge, albeit from a low base, to reach US$133.52 million, while the Americas notched a 5.2% growth to US$264.15 million. Europe maintained a flat trajectory, inching up 0.72% to US$920.74 million.

Chart 1: Shariah real estate assets by region, AuM and fund count

Chart 2: Shariah real estate assets by country, AuM and fund count

Table 1: Global Shariah asset base changes, q-on-q

| Region | Q4 2025 (AuM in US$ million) | Q1 2026 (AuM in US$ million) | AuM change |

| Africa | 41.71 | 133.7 | 220.53% |

| Americas | 250.98 | 264.13 | 5.24% |

| Asia Pacific | 8,351.32 | 8,653.24 | 3.62% |

| Europe | 914.13 | 920.74 | 0.72% |

| Middle East | 15,259.92 | 14,409.25 | -5.57% |

| Grand Total | 24,818.06 | 24,381.07 | -1.76% |

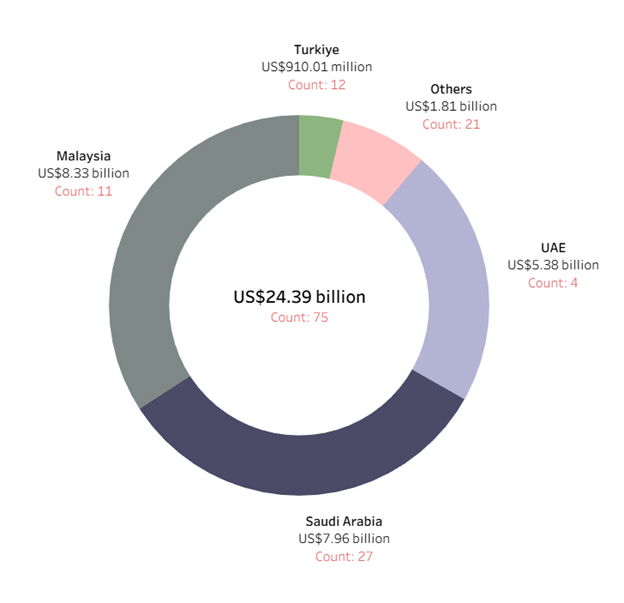

Malaysia’s KLCC REIT leads in AuM

A closer inspection of individual fund alignments in the Shariah real estate landscape for Q1 2026 shows how these regional flow revisions have reshaped the global corporate hierarchy.

In a historic shift at the top of the individual fund rankings, Malaysia's KLCC Property Holdings’ KLCC REIT seized the crown as the world's largest capitalized public Shariah property fund, surpassing UAE giant DHAM REIT Management′s Dubai Residential REIT.

Benefiting from Asia Pacific’s broader capital momentum, the KLCC REIT advanced its capitalization q-o-q to US$4.83 billion from US$4.7 billion. Dubai Residential REIT’s AuM shrank to US$4.18 billion from US$4.78 billion q-o-q.

Other core vehicles across the Islamic property universe maintained stable, defensive positions amid the volatility. Axis-REIT Managers saw its flagship vehicle anchor the third position at US$1.34 billion, followed closely by Pelaburan Hartanah′s Amanah Hartanah Bumiputera at US$1.26 billion.

Within the GCC, Equitativa Group’s Emirates REIT provided a steady institutional baseline with an AuM of US$896.1 million.

Table 2: Global Shariah real estate funds ranked by AuM

| Rank | Fund | Manager | AuM (US$ million) |

| 1 | KLCC REIT | KLCC Property Holdings | 4,826.76 |

| 2 | Dubai Residential REIT | DHAM REIT Management | 4,177.08 |

| 3 | Axis-REIT | Axis-REIT Managers | 1,343.89 |

| 4 | Amanah Hartanah Bumiputera | Pelaburan Hartanah | 1,255.28 |

| 5 | Emirates REIT | Equitativa Group | 896.1 |

| 6 | Al Rajhi REIT Fund | Al Rajhi Capital | 848.59 |

| 7 | Jadwa REITs Fund | Jadwa Investment | 759.24 |

| 8 | Jadwa REIT Saudi fund | Jadwa Investment | 744.32 |

| 9 | Bonyan REIT | Saudi Fransi Capital (BSF Capital) | 581.84 |

| 10 | AlAhli REIT (1) | SNB Capital | 529.71 |

Turkish funds still lead performance, but with smaller returns

Short-term fund returns reinforce the narrative of a cooling market within traditional growth hubs, giving way to more deliberate risk management strategies. Turkish property vehicles, which formerly dominated performance charts with returns scaling above 30% via managers like Ziraat Portfoy, have adjusted to the broader market cooldown.

According to the performance metrics for Q1 2026, the Albaraka Portfoy Real Estate Participation Short Term Participation Free (TL) Fund secured the top global return ranking, delivering a 9.16% gain.

Ziraat Portfoy’s Basak Participation Fund captured the second position with a 6.38% return, just ahead of JLG REIT Managers’ Al-'Aqar Healthcare REIT, which yielded a steady 5.57%.

Global Shariah real estate funds, ranked by 3-month return

| Rank | Fund | Manager | Three-month return (%) |

| 1 | Albaraka Portfoy Real Estate Participation Short Term Participation Free (TL) Fund | Albaraka Portfoy | 9.16 |

| 2 | Ziraat Portfolio Management Basak Participation Real Estate Investment (TL) Fund | Ziraat Portfoy | 6.38 |

| 3 | Al - 'Aqar Healthcare REIT | JLG REIT Managers | 5.57 |

| 4 | Tera Portfolio Management Housing Alfa Participation Real Estate Investment Fund | Tera Portfoy | 4.19 |

| 5 | Al Rajhi Real Estate Monthly Distribution Fund | Al Rajhi Capital | 3.98 |

| 6 | Markaz Real Estate Fund | Markaz (Kuwait Financial Center) | 3.58 |

| 7 | SNB Capital Fund of REITs Fund | SNB Capital | 2.78 |

| 8 | Global Sharia REITS Portfolio | Invesense Asset Management | 2.1 |

| 9 | Albilad Fund of REIT Fund | Albilad Capital | 1.89 |

| 10 | HSBC FTSE EPRA NAREIT Developed Islamic UCITS ETF | HSBC Asset Management | 1.69 |

Outlook

The immediate trajectory for Shariah property allocations points toward a more calculated, sophisticated approach to geographic risk.

While the macro adjustments observed in early 2026 reflect a tactical pause within traditional core GCC markets, they do not signal a permanent retreat.

Instead, institutional capital is pivoting toward a dual-track strategy: maintaining baseline exposure in high-conviction Gulf assets while actively chasing growth across highly liquid Asian and specialized African hubs.

The long-term performance landscape confirms that market volatility is yielding highly localized opportunities for alpha. Managers that can successfully pair rigid Shariah compliance with the structural advantages of listed REITs – namely dividend predictability, operational transparency and secondary market liquidity – will remain the primary beneficiaries of global capital flows. As the broader ethical investment universe scales, these institutionalized property vehicles are well-positioned to transition from defensive hedges into primary drivers of cross-border wealth creation.

Restricted Access

Login to continue reading (existing subscriber)

Subscribe NOW and get:

- Gain unlimited access through all key operating platforms

- Full access to all listed Islamic funds & fund profiles

- Unlimited access to all Islamic fund managers

- Access to all exclusive articles, reports, podcasts & videos

- Complimentary access to all IFN Investor Forums